|

How do you achieve sustainable growth in investing? One needs to choose those leading companies that are prepared to provide strong, consistent and long-term increases in profits and revenue. These are the firms that reward their shareholders with above-average market returns.

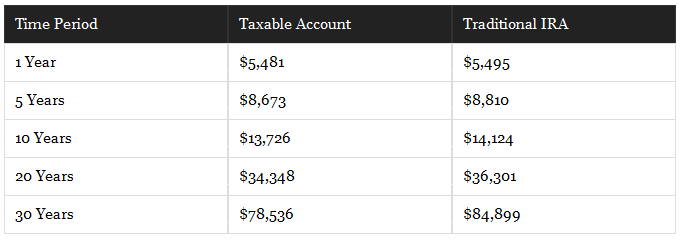

Apply these tips coming from some of the most experienced investing leaders. See how you, too, can discover the latest winning growth stocks and, thereby, make a fortune for yourself. 1. Go for Quality The best investment choices are often the best businesses you can find. David Gardner, popular investor and co-founder of Motley Fool says, "I look for the excellent, buy the excellent and add to the excellent in time. However, what I sell is the mediocre. That is my investment style." Quality companies possess the most powerful competitive edge, the widest market potentials and a top-of-the-line management. They know how to be creative, trend-setting and pioneering. Most of all, they can build wealth for their shareholders and lead others to achieve their dreams. 2 & 3. Jump in as early as you can; and grab that basement-price offer You can maximize your profit by investing early in a great business as more investors join in the harvest. Wealth abounds for those who practice this principle – especially for the 10- and also the 100-baggers – bringing on life-changing gains. Nevertheless, many investors frequently hesitate to enter into the early-stage surge of best growth company stocks because they appear pricey, only to regret having missed the opportunity to gain in the end. While buying stocks in these quality businesses at high prices is an option, we can decide to go ahead and pay the premium for a quality acquisition. Setting your targets too low or just a notch or two below the optimum level might cause you to lose the opportunity to hit a multi-bagger. 4. Invest on a long-term duration Warren Buffett puts it this way: "My favorite holding period is forever." CEO and master investor, Tom Gardner, in fact, has established at Motley Fool at least a five-year holding time rule in an Everlasting Portfolio since he adheres to the effectiveness of holding stock on a long-term basis. In David Gardner’s words, as a prime mover of one of the most efficient high-growth investment-consultancy services in the world, the heart of this investment approach consists of “two keys. . ., stock by stock: In before the big majority of people, and out after the big majority of people”. Aiming to buy stocks in businesses and holding on to them for years or even decades allows the power of tax-deferred compounded returns to our advantage. 5. Those who win keep on winning Tom and David Gardner reveal another winning advice: Invest in businesses and management groups with unequalled track record of success. In their tweeted message, they say: “Our take on that famous disclaimer: ‘Past performance’ may turn out to be the single *best* determinant of future results we have can.” Although it is not guaranteed, winning can be made into a habit. The force of momentum and the trusted experience developed in past successes tend to favor those who continue to face investment risks. And we do not refer to foolhardy risk-taking based on pride, but well-informed, facts-based choices born out of positive and strategic projections of a fruitful future. 6. Let your portfolio speak your best to the world David Gardner once gave this valuable advice: "Determine where the world is headed; and as soon as you can, get there." Your portfolio speaks of your aspirations, interests, specialization and profession – that is where your advantage lies. Above all, your portfolio runs parallel to the trajectory of your vision of the future—and with a more positive view, the clearer the vision is. 7. Do not give up the fight Growth investing can be frustrating at times; there will be moments when you harbor doubts and want to give up. Certain inexplicable short-term fluctuations and extreme bear market dips may wreak havoc on top-quality yet usually high-priced growth stocks, taking a toll on your emotions. Ultimately, the only path to success is to remain steadfast throughout any undesirable turn of event. “The short-term will not teach an investor to learn enough – usually in a significant way -- to be so successful in the long-term,” according to Tom Gardner. Be assured with the knowledge that everything will pass and, thus, you must expect the big-league companies to come out victorious after the dust clears up, remaining stable while the rest of the bunch lose their market share. With that in mind, consider such sell-offs as potential moments for strengthening your positions at even higher prices and enhancing your long-term returns. For beginners as well as veterans in IRA investing, here are a few important things to consider. Newbie investors obviously need education in fundamental matters while long-time investors can always benefit from new ways to enhance their investment strategy. So, how do you maximize returns from your IRA? Choose what fits your goals: Traditional or. Roth Should you go for traditional or for Roth IRA? While your traditional IRA contributions can be classified as tax-deductible, Roths use after-tax money; however, they provide tax-free withdrawals when you reach retirement age. To know more about either type of IRA, visit informative investment websites. Here are a few valuable tips on which to choose: When you should choose a traditional IRA: · If you are within a higher tax bracket now, in contrast to your expected level when you reach retirement · If a tax break now is more preferable to you than tax savings when you retire · If you have no retirement plan sponsored by your employer because your income is too large to qualify you to directly contribute to a Roth IRA When you should choose a Roth IRA: · If you want to stay in your present tax rate · If you want to diversify your retirement assets, aside from your pre-tax account such as a 401(k) · If you expect to use the money when you retire and would choose rather to keep it in that account to allow it to grow as long as you want (A Roth IRA will not demand a minimum distribution from a specific age.) · If you want all your money safely parked somewhere (You can withdraw your original contribution amounts in a Roth IRA at any time.) Take full advantage of the tax benefits To maximize returns from your IRA, choose the most appropriate types of stocks. Whatever stock whose value grows in time will provide higher gains for you in an IRA compared to a taxable brokerage account. Nevertheless, dividend-growth stocks will optimize the entire compounding capacity of investing in IRA; hence, you must utilize your IRA through buying individual stocks. As an example, with two stocks often favored in many portfolios, such as Berkshire Hathaway and Apple, one can assign one in a traditional IRA and hold the other in a taxable brokerage account. Invest $5,000 in each one of these two accounts. As of today, Apple pays a 1.9% yield in dividends, generating $95 from your $5,000 investment for a year. You will be charged a 15% tax in a taxable brokerage account, effectively giving you about $81 return. However, in a traditional IRA, you get a tax-free deal. Remember: You can now reinvest the entire $95 in more shares, whereas you have less to put back in a taxable account to work with. Although $14 is not that much, the compounding power of money works more in the former than in the latter, especially in the long-term. To illustrate more clearly, under a 1.9% dividend yield for Apple and a stock gain of 8% annually, you will observe the difference in the gains of an initial investment of $5,000 over time:  Your returns are more obviously higher over a longer period of time than otherwise, as seen in the difference above after 30 years. A $6,400 advantage, more or less, in a traditional IRA is definitely more preferable.

A $5,000 investment in Berkshire Hathaway, in comparison, would only take advantage from an initial tax deduction on your IRA contribution. As Berkshire has no dividend-yield payments, your investment in both kinds of accounts will grow by a fixed amount over time. The young should invest aggressively now Allocating too little money or not investing at all could be the worst mistake anyone can make in IRA investing, especially among young investors. It is natural for millennials to be wary of investing in stocks, considering the early-2000s’ tech crash and the more recent Great Recession, and since many of these millennial investors had parents who lost their investments in the market. You can use an accepted rule of thumb to determine the percentage of stocks to be included in your portfolio by deducting your age from 110. For instance, if you are 40, around 70% of your money invested must be in stocks. Using this principle will allow your portfolio to become more conservative as you near the retirement age. It is likewise worthwhile to note that ETFs and stock-based mutual funds can serve as good alternative investments if individual stocks do not appeal that much to you. Just remember that stock investments will always involve volatility. Hence, in any particular year, a 10% drop in the stock market should be expected. Nevertheless, on the long-term, stocks will provide better gains compared to any other types of assets. Lastly, most of all your investment money will never acquire greater growth opportunity in the long-term than they do in the present, no matter what happens to the market this week or this year. At 25, according to a conservative average of 7% annual growth rate over many years, one only has to invest $5,000 each year ($417 every month) to become a millionaire-retiree at 65. However, at 35, you need to set aside $15,800 each year, or $1,318 monthly, to reach the same level of wealth at 65. In short, invest as much as you can and as early as you can since time is your most valuable asset, aside from your dollars.  Back in 1997, the U.S. government issued Treasury Inflation-Protected Securities (TIPS), which are backed by the credit and full faith of the government and guarantees that their value will not be eroded by inflation; thus, providing risk-free asset for investors in the U.S.

Both TIPS face value and coupon payments are indexed to keep up with inflation and to protect buying power, while their returns are set in real inflation-adjusted terms. Under positive inflation (versus deflation) conditions, actual returns are below the nominal gains quoted on traditional (without inflation adjustment) bonds. Estimating for the real interest rate, we get: real interest rate = nominal interest rate - expected inflation rate Or, to be more exact, the actual formula using these variables will be: (1 + nominal interest rate) = (1+ real interest rate) * (1 + expected inflation rate) We determine nominal interest rates by adding the compensation expected to keep up with inflation and a real interest rate of return for the investment. Surely, bond prices and interest rates can be impacted by supply and demand. And real interest rates may take a negative value, as mentioned above. Of course, investors hope for a positive nominal return on investment (the very reason for investing, obviously); however, the gain might not catch up with the inflation rate. TIPS, compared to conventional bonds, provide returns which are quoted as real interest rates. TIPS nominal returns cannot be predicted in advance since they are determined by the actual inflation experienced. It also follows that nominal returns can be determined for conventional bonds; however, their real returns can only be determined after monitoring the realized inflation track until the maturity date. Adjustments of inflation for TIPS are set to the Consumer Price Index for All Urban Consumers (CPI-U). Such adjustments are observed according to the “accrued principal,” a dedicated term used for TIPS. Accrued principal is the value after due adjustment for inflation of the original face value at the time the TIPS was issued. Inflation adjustments for TIPS are achieved through the coupon rate being paid on the accrued principal value, not on the value of the nominal initial face. Likewise, during maturity, the investor gets back the accrued principal, not the nominal face amount. An inflation-adjusted value is paid at a real coupon rate and an inflation-adjusted value is paid at maturity. During deflation, the accrued principal can go down; however, it is protected against dipping below its original par value. What this signifies is that TIPS on the secondary markets having lower accumulated principal can provide higher protection during deflation, considering all other factors unchanged. On the other hand, deflation that is not substantial enough to make the accrued principal to drop below its original par value will adversely affect TIPS in relation to conventional bonds. As a general rule, the goal of TIPS is to protect investments from unpredictably high inflation; thus, acquiring TIPS with a lower relative accrued principal is a supplementary factor in selecting certain TIPS to buy. TIPS are available in nominal dollars. The ask price for TIPS on the secondary market is set in real terms, quoted as a percentage value of the accrued principal after adjustment for inflation. The actual price paid is computed as the ask price multiplied by the accrued principal, then divided by 100. Since 1997, TIPS bonds and notes have been issued. From that time until the middle of 2002, every TIPS auction covering different maturities yielded an initial real return over 3%. Fortunate investors in 1998 and 1999 could have acquired 30-year TIPS giving almost 4%, while 10- and 20-year TIPS gains were more than 4% in 1999 and 2000. TIPS yields have dropped since then. A TIPS auction for a five–year note conducted in October 2010 made news as the real yield dropped below zero (at negative 0.55%) only for the first time. Buyers of such issues have resigned themselves to returns not protected from inflation. Although unusual then, negative returns for TIPS have recently become a more common occurrence nowadays.  Inclement weather has the surprising advantage of giving us time to spend quality time indoors and deal with our finances. Even the most innocent questions from a nervous friend, if she is doing the right thing or not or where to check her credit score eventually, turned into the issue of what to do next.

Everyone going through the “growing-up blues” needs the assurance that the things she was doing and bringing her anxiety made her a better person every step of the way. The key is finding out how to begin effective financial planning. Here are some helpful steps to follow: Do not be anxious Although you might not end up choosing the most beneficial funds for your retirement plan or you end up paying for a credit score instead of getting it for free or you paid a slightly higher interest rate on your loan than you wanted, you will still be way ahead by a long stretch compared to having done no planning at all. Granted, everyone wants to have the best choices for optimizing benefits and savings; however, fretting over how to chase the “highest and best” and ending up being paralyzed is counterproductive. The better goal to aim for is TIME. It is a commodity you cannot renegotiate or purchase back. Do with what you already have Determine where you are exactly before making a plan for your future by calculating the figures that that tell you what you have and what you need to have. Do a financial inventory first – net worth, account balances, credit score, liabilities and assets. Consolidate all your finances using Personal Capital’s free tracking application in order to obtain a complete perspective of your financial status at any time. Direct your course Look at your finances as a road map, telling you where to put location markers along the way as you travel and to direct your destination. Only by marking your origin and staking out your destination will you be able to determine the most efficient route from one point to the other – and that is how finances work as well. Set your goals, your time frame and the cost for every step of the journey and order them according to their urgency. Get educated on how you can effectively set and achieve goals through online aids that help you how to remain organized and to monitor your progress. Marking your direction Your present financial assessment marks your starting point and your goals as your destination, while your budget is your direction on the map. And before you can even begin to take the trip on that map, you must draw your direction – that is, make a budget. Create a budget that best suits your situation -- a percentage budget, a zero sum budget or a cash- only budget – making sure that you stay above your make-or-break level, meaning your minimum cost of living, including savings. By diligently minimizing your spending to essential expenses and/or maximizing your income in order to reach and go above the essential level, you will begin making headway. Read on the article “How to make a budget without a budget”. What now? Having done your inventory and determined your minimum financial level, you can have a better idea of your leftover money in order list your prioritized objectives. Where do you start? Should you pay off your loan? Or save into a retirement account? Open a savings account for a down payment for a home? Increase your emergency fund? With so many needs and not enough money, what is one to do? At this point, the “growing-up blues” set in. Relax and be not anxious – no matter what happens, as long as you make reasonable choices, the road will lead you home. Categorizing Financial Goals There are four major categories of financial goals: · Emergency savings · Loan payment · Short/Medium-term savings · Long-term/Retirement savings Most experts recommend funding all of these goal categories, aside from covering your monthly costs, and assigning bigger income portions to your highly-favored goals. However, rarely do things work your way and your limited income may require you to choose one or two financial goal categories above the rest. Oftentimes, the two most crucial are emergency savings and loan payment. Providing yourself a safety net at a minimum of $1,000 is the first on your list (although the target amount should be enough to cover your living expenses for about 6 months). With your 1k emergency fund, proceed by distributing your money accordingly for emergency savings contributions and loan payment. You may also want to insert a tiny amount for your retirement savings into the picture -- this could be as small as $50 monthly – which is good enough for a low-interest debt. Also, remember to contribute to short and medium-term fund savings. For young professionals, you have enough time before you reach 59½ to set aside some money for your lifelong dreams, whether a dream house, raising a family, travel, etc. That refers to money apart from your retirement nest egg or emergencies funds. However, if your budget will not allow you to contribute to all savings categories, your best solution is to seek ways to increase your income. Saving money and reducing your daily expenses can only do so much. Your ability to earn more has practically no limit whatsoever; and having the flexibility and freedom that greater earnings provide will further enhance your financial and life aspirations. Financial experts will attest to this fact. Financial Planning for Novices Review · Assess your financial situation · Set your goals · Make a budget and surpass your minimum cost of living · Prioritize your objectives and set aside surplus money from your living cost · Enhance your income generation for funding higher targets · Relax and enjoy your accomplishments Breaking it down to the barest components, novices can do effective financial planning using a few essential, practical steps, namely: earn more money, reduce expenses and set aside extra money consistent with your highest goals. Following these vital tips is your best weapon against the onset of “growing-up blues”.  Were you a victim of the holiday spending spree this past season or a winner? Many of us lost; and the New Year gives us pause to evaluate our personal financial habits once more and, hopefully, initiate some positive and lasting changes for the future.

Consider these valuable saving and spending hacks you can implement. Go long-term Think ahead into the future. Whatever your age is, save now for your retirement. The earlier you do, the better. Apply for an employer-sponsored plan, if possible. Or if you can, opt for IRAs which help you build wealth in bounds. Build categorized funds Think of this as a challenge: Do the 52-week savings procedure. Set aside $1 on the first week, then $2 the second week, until you finish the 52nd week, when you are supposed to add $52 to your pot. Hacking this process gives you $1,378 in savings in the next year, plus interests earned. As long as you set for yourself a specific goal, starting a savings account can bring great benefits. Go for banks that offer fee-friendly services, such as Ally Bank Member FDIC, ally.com, which enables you to open an Online Savings or Money Market account without minimum savings requirement or monthly service charges. It is quite convenient to deposit money through an e-check deposit, direct deposit and you gain compounded-daily interests on your savings. Moreover, keeping this money in a separate account lets you monitor your spending habit versus the remaining balance. Utilize shopping apps It has become quite easy to save money using online apps. Do some research and find discount codes, loyalty plans or cash-back providers that allow you to monitor your expenses and reward you for the use of their shopping portal instead of going directly to the big name retailers’ homepage. Gain rewards Although it is downright risky and even foolhardy to run up credit-card bills one cannot pay back, many expert consumers have the ability to exploit credit card reward plans for airline mileage, hotel points or hard cash on-hand. “Utilize credit cards that offer reward for things you often purchase,” says Diane Morais, chief executive officer and president of Ally Bank, subsidiary of Ally Financial Inc. Open a new credit card which provides a minimum buying limit, such as the Ally CashBack Credit Card, which offers a $100 bonus when you spend $500 in eligible purchases within the first three billing cycles, and gives 2% cash-back at gas stations and grocery stores, as well as a 1% cash-back on all other purchases – including 10% bonus on rewards which you deposit into a qualified Ally Bank account. It is not necessary to open a new account if your present credit cards to avoid fraud and also offer promos or cash-back schemes, allowing you to earn substantially on daily purchases. Consider the above tips and aim to become a strategic consumer – one who spends wisely and saves productively.  If you are like me, you probably worry a lot about being caught in an investing trap. I am a recent player in the investment industry, with my only accomplishment being able to max out my IRA each year. I do not have a Plan B for my investing strategy; so I have tried to educate myself about other ways of investing in order to invest more actively or, at least, fortify my ongoing investments this year.

Many young professionals do not know for sure how to invest their money, except for their 401(k). If you are one of those clueless individuals, check out these novice tips to help you achieve your resolution to become a better investor this year. Investment expert Hans Scheil, the president of North Carolina-based Cardinal Retirement Planning, Inc. and author of The Complete Cardinal Guide to Planning for and Living in Retirement will help us understand these principles. By the way, he is a 40-year veteran in the financial services area, helping investors build a diversified and sound investment portfolio. 1. Invest only beyond your 401(k) and IRA if you have reached your limit in your contributions. Scheil emphasizes that deciding to invest beyond a 401(k) or IRA should only be considered when you have reasonably maxed out your retirement accounts. He says, "This is because of income taxes. You cannot pass up deferred tax or even free tax benefits. Firstly, plan and decide how much you need to invest, where the [extra money] is coming from (a bonus, regular income, asset sale, inheritance, gift, savings account money, etc.), when you may have to use it or when you want the money, and how much risk you can withstand.” 2. Avoid focusing on daily market fluctuations. “New investors often focus on daily market cycles and timing the investing process. You will never enter at exactly the right time or exit at exactly the right time. Averaging dollar cost or investing at regular periods will tend to balance out the highs and lows,” says Scheil. The guiding principle is that if you are between 25 and 35, the market movements on any particular day will not overly affect the retirement money you expect to get 30 years after. 3. Before considering other investments, first understand completely your present portfolio. Scheil offers a diagnostic list of questions to assess your situation: “When you have extra money to invest, I recommend a quick evaluation of your current portfolio. Do you have a balanced diversification? Does your investment standing address your set goals? Do your investments perform reasonably against actual risks and the market conditions? Knowing the exact answers to these questions will help you decide if you should use your extra money into your existing investments.” 4. What you might actually need is not opening another account. Regarding three various kinds of investments, Scheil gave these comments (These are his personal views; other experts may have other opinions, obviously.): To open or not to open another account - “You need a new investment account only if it is has a different name on the account or has a different tax status.” To invest or not to invest in a particular business - “I recommend diversification only if you personally own and manage the specific business you invest in.” To invest in real estate or not - “Investing in real estate is advantageous in a portfolio to serve as an optional investment with a stocks portfolio, up to a certain proper amount. Owning real estate yourself is great as well; however, it might end up difficult to sell and burdensome to handle.” 5. If you are considering new investments, determine what will succeed in 2040-2050. According to Scheil, the most appropriate choice for millennials wanting to improve their investing potential is to “remain in the stock market for the long-term and consider buying during market dips”. Likewise, he strongly suggests that we think hard about what will gain long-term value when dealing with stocks. “Be guided by this simple test: What will be very valuable in the year 2050? What will earn a lot from now up to 2050? Renewable energy, bio-technology, goods and services for the elderly, products in demand in growing economies and other potential goods are viable choices,” says Scheil. "Moreover, companies, such as Apple, Google, Tesla, CISCO, Amgen and CVS, present golden opportunities.”  Part of the yearly ritual for the yuletide holidays among many people is that of evaluating their budget to avoid overspending during the last few months of the year. This is always a good practice; however, why do it only for the last part of the year? Extend the habit and deal with your 2017 budget.

If you are up to it; then, get a calendar, open your spreadsheet, or any kind of system you want to use and let us work together on your budget. Consider these tips on how to go about it. • Prepare for Changes – As early as you can, anticipate changes, such as a college tuition fee or a new home mortgage. Include these expenses in your budgeting plan beforehand even you are not certain as to the final amount required. Taking a long time to find out the exact value for such expenses may disrupt your other important expenses. On the other hand, you could be expecting welcome changes which you must include in your planning, such as a expected salary increases, bonuses and commissions. • Be Conservative in Your Estimates – When anticipating the value of a certain future expense, make conservative projections. Add a certain percentage to the expected expenses while subtracting the same percentage from anticipated income raises or commissions. Although most people do not consider this prudent, being conservative provides a buffer in case the future turns out to be contrary to your expectations. Always expect staple expenses such as utilities, groceries and gas to increase as they always do. At it stands, a 2% increase will cover inflation in majority of regular expenses. However, gas and utilities should be given a higher expected rise since they are hard to predict whether in terms of usage and price. • Evaluate Previous Results – Before the year comes to an end, you should already have a very good conception of the objectives you wish to achieve for the year and which goals you will not achieve. Based on your evaluation, you may have to slow down on your expenses, augment your savings, reduce your debt or make necessary changes accordingly. This recommendation also applies to your method of monitoring and distributing your budgetary expenses. Do you have difficulty finding out if you achieved your financial objectives? And you have to tear your budget and make a new one each month? Try juggling your budgeting strategy. Try this: When you find yourself always failing to meet your savings target, resort to the “bucket” method. Assign portions of your income to designated buckets, such as one for monthly expense and another for fixed monthly expenses such as rent/mortgages and also one for discretionary funds. Allocate funds for the monthly expense and savings buckets prior to your discretionary funds. • Assign New Targets – Adjust your objectives according to your evaluation and recommended changes. For instance, you may want to speed up your savings to address a down payment need for a home purchase, while preparing for interest fees to go up in the following year (which is a probable event, in our opinion). • Make Necessary Changes in Your Budget – When you are finished with your amended objectives and assumptions, change your budget to cover the following year’s conditions. Having a monthly budget suits the situation for many people; but you can pick an appropriate schedule that suits your unique lifestyle. Is it proper to project a budget for 2018? Not really. No one has enough information to project that far ahead. Nevertheless, you should consider forward-looking expenses, purchases and salary increases in your present budget. For instance, if you are expecting to spend for a college education in 2020, the best time to prepare for it is not later than today. You should congratulate yourself for deciding to get ahead of the race and planning the New Year’s budget before most people even think about it. Half the battle is already won, in your case. Develop the discipline to follow your plan for the entire year as much as you can. That is how you win the other half.  At Bellmore Group, we regard our culture to be among our many creative outputs. Bellmore Group have painstakingly developed through many years our culture into what it is at present - a venue for conceiving and creating ideas into realities. Today, that culture has produced unity among our workers and business associates throughout the world.

Bellmore Group Investment Company Holland Hills Mori Tower 19F 5-11-1, Toranomon, Minato-ku, Tokyo 105-0001 Japan Phone: +81 3 4589 4990 Email: [email protected] Website: www.bellmoregroup.com  1. Terms

By accessing this web site, you are agreeing to be bound by these web site Terms & Conditions of Use, all applicable laws and regulations, and agree that you are responsible for compliance with any applicable local laws. If you do not agree with any of these terms, you are prohibited from using or accessing this site. The materials contained in this web site are protected by applicable copyright and trade mark law. 2. Use License a. Permission is granted to temporarily download one copy of the materials (information or software) on Bellmore Group's web site for personal, non-commercial transitory viewing only. This is the grant of a license, not a transfer of title, and under this license you may not: · modify or copy the materials; · use the materials for any commercial purpose, or for any public display (commercial or non-commercial); · Attempt to decompile or reverse engineer any software contained on Bellmore Group's web site; · remove any copyright or other proprietary notations from the materials; or · transfer the materials to another person or "mirror" the materials on any other server. b. This license shall automatically terminate if you violate any of these restrictions and may be terminated by Bellmore Group at any time. Upon terminating your viewing of these materials or upon the termination of this license, you must destroy any downloaded materials in your possession whether in electronic or printed format. 3. Disclaimer a. The materials on Bellmore Group's web site are provided "as is". Bellmore Group makes no warranties, expressed or implied, and hereby disclaims and negates all other warranties, including without limitation, implied warranties or conditions of merchantability, fitness for a particular purpose, or non-infringement of intellectual property or other violation of rights. Further, Bellmore Group does not warrant or make any representations concerning the accuracy, likely results, or reliability of the use of the materials on its Internet web site or otherwise relating to such materials or on any sites linked to this site. 4. Limitations In no event shall Bellmore Group or its suppliers be liable for any damages (including, without limitation, damages for loss of data or profit, or due to business interruption,) arising out of the use or inability to use the materials on Bellmore Group's Internet site, even if Bellmore Group or a Bellmore Group authorized representative has been notified orally or in writing of the possibility of such damage. Because some jurisdictions do not allow limitations on implied warranties, or limitations of liability for consequential or incidental damages, these limitations may not apply to you. 5. Revision & Errata The materials appearing on Bellmore Group's web site could include technical, typographical, or photographic errors. Bellmore Group does not warrant that any of the materials on its web site are accurate, complete, or current. Bellmore Group may make changes to the materials contained on its web site at any time without notice. Bellmore Group does not, however, make any commitment to update the materials. 6. Links Bellmore Group has not reviewed all of the sites linked to its Internet web site and is not responsible for the contents of any such linked site. The inclusion of any link does not imply endorsement by Bellmore Group of the site. Use of any such linked web site is at the user's own risk. 7. Site Terms of Use Modifications Bellmore Group may revise these terms of use for its web site at any time without notice. By using this web site you are agreeing to be bound by the then current version of these Terms and Conditions of Use. 8. Governing Law Any claim relating to Bellmore Group's web site shall be governed by the laws without regard to its conflict of law provisions. General Terms and Conditions applicable to Use of a Web Site.  Investing in stocks to help you achieve your financial objectives

In terms of stock investing, understanding your financial objective is critical. That, together with your investment time targets and your risk capacity when investing in stocks, will aid you in determining how your stock investments should perform with the rest of your financial portfolio. When to consider investing in stocks Stock investing can enhance your financial portfolio by allowing you to attain growth, profit from dividends or achieve both. Nevertheless, the worth of any stock you buy in can vary, and when you sell your stock, may be more or less than what you paid at the start. When choosing stocks to buy in, you should cautiously reflect on the risks of investing in stock and design an assorted asset allocation strategy that suits your objectives, investment time target and risk capacity. Diversifying your stocks Having a varied stock portfolio helps to offset the risk your investments are subjected to. The objective is to widen the range of your stock investments among various sectors and incorporate various investment characteristics so that when a certain stock or sector does poorly, the performance of your stocks in other sectors may aid in offsetting the changes in the overall worth of your stock portfolio. Some basic guidelines you can utilize when selecting a variety of stocks for your portfolio are: • Invest in about 20 to 30 stocks in a minimum of six to eight sectors with various investment characteristics. • Limit to only 25% of the overall worth of your stock portfolio should be in any particular sector. • Limit to 15% of the overall worth of your stock portfolio should be in any particular stock. • You need to invest at least about 3% to 4% of the overall worth of your stock portfolio in every stock. • Your investment counselor can assist you in designing a mixed financial plan that fits your circumstances and your financial objectives. |